After the Announcement: A Financial Planning Guide for People in Transition

Most of the hardest financial decisions in a person's life arrive on the same day as the news.

The severance letter has a signature deadline on it. The divorce filing starts a clock you did not set. The call from the hospital is followed, sometimes within days, by questions about accounts and beneficiaries and what happens to the paycheck. The transition shows up as an event, with a date, and the money decisions are stapled to it whether you are ready or not.

That is the part almost nobody prepares you for. Not that the decisions are complicated, though some of them are. It is that they land at the exact moment you have the least capacity to make them well. You are grieving, or angry, or scared, or just exhausted, and someone hands you a form and asks you to elect something irreversible by Friday.

I have sat across from hundreds of people in that moment. What I have learned is that the financial pieces and the emotional pieces get tangled together, and that untangling them is most of the work. You cannot think clearly about a lump-sum versus installment severance election while you are also processing that the job you built your identity around is gone. Nobody can. The two problems feel like one problem, and it is overwhelming.

So the goal of this paper is narrow and specific. It is to pull the financial pieces out from under the emotional ones, lay them on the table, and show you how to think about them. Not so you feel nothing. So that you can handle the money part with a clearer head, and give the human part the room it actually needs.

I have organized this around a simple idea: the first ninety days matter more than any single decision inside them. Get the sequence right, protect yourself from the choices that cannot be undone, and almost everything else can be handled at a pace you can live with.

The First 90 Days

Every transition I have worked through has the same shape underneath the specifics. There is a burst of decisions right at the front, most of them feeling urgent, a handful of them actually urgent, and a small number that are both urgent and permanent. The single most useful thing you can do in the first ninety days is tell those three groups apart.

So before anything else, sort every financial decision in front of you into one of three buckets.

Has a real deadline. Something outside your control is forcing the timing. A severance agreement with a signature window. A COBRA election with a 60-day clock. A deferred compensation distribution election that locks the day you separate. An estate account that has to be opened before other things can move. These are the decisions that can genuinely hurt you if you miss the window, and they are the ones that deserve your attention first. The good news is there are usually fewer of them than it feels like.

Can wait, and should. Most of what feels urgent belongs here. What to do with the 401(k). Whether to keep or sell the house. How to invest the settlement or the proceeds or the insurance payout. Whether to move, change careers, or restructure your whole financial life. These feel pressing because everything feels pressing right now, but almost none of them have a real clock on them. Money sitting in a savings account or a money market for ninety days while you get your feet under you is not a mistake. It is a strategy. The cost of waiting is a little bit of yield. The cost of deciding badly is far larger and often permanent.

Should never be decided in the first month.

This is the bucket people forget exists. There are decisions that are technically available to you immediately but should be actively refused until the fog lifts. Any large irreversible move made from grief, anger, or fear belongs here. Paying off a mortgage in a single lump because the uncertainty is unbearable. Gifting money to family in the emotional rush after a death. Making a dramatic investment change because the market moved and your stomach cannot take it on top of everything else. The rule I give people is simple. If a decision is both large and permanent, and nothing external is forcing it, it waits until you are steadier. There is no financial upside large enough to justify making a one-way-door decision while you are underwater.

Once you have sorted the decisions, the work of the first ninety days is mostly protection, not optimization.

Protect your cash position. Before you do anything clever, make sure you know what is coming in, what is going out, and how many months of runway you have. A transition almost always changes the income side of the ledger, sometimes overnight. Rebuild the picture on the new terms. Knowing you have eight months of expenses covered changes how every other decision feels. Anxiety about money is often anxiety about not knowing, and the number is knowable.

One of the most common things I hear in a first meeting during a transition is some version of "I have no idea if I'm going to be okay." Almost every time, we sit down, build the actual picture, and the person is more okay than they feared. Not always. But the fear is almost always bigger than the number, because the fear fills the space where the number should be. Putting a real figure on the runway does not solve the problem. It shrinks it to its actual size, which is usually survivable.

Protect your coverage. Health insurance is the one that catches people. When a job ends, coverage often ends faster than expected, and the COBRA-versus-marketplace decision has a real deadline attached. When a spouse dies, the surviving partner's coverage may have been running through the other person's employer. Do not assume you are covered. Confirm it, in writing, in the first two weeks.

Protect the paperwork. Beneficiary designations, account titling, and access. After a death or a divorce especially, the person named on an account and the person who should be named are often no longer the same. These are quiet problems that do not announce themselves until it is too late to fix them cheaply. A one-hour review in month one prevents a genuine mess in year two.

Notice what is not on this list. There is no investment strategy here. No tax optimization. No grand financial plan. Those things matter, and we will get to them, but they are month-four problems dressed up as month-one problems. The temptation in a transition is to do something big and decisive so you feel back in control. Resist it. The people who come through these moments in the best shape are almost never the ones who moved fastest. They are the ones who protected themselves early, refused the permanent decisions, and gave themselves permission to handle the rest at a human pace.

There is a reason I put the permanent decisions in their own bucket. I worked with someone who, three weeks after losing her husband, wanted to pay off the house in full. The money was there, and the certainty of it felt like the one solid thing she could grab onto. There was nothing wrong with the idea on paper. But nothing was forcing it, and she was not in a state to be making a permanent decision with a large chunk of her liquidity. We agreed to revisit it in ninety days. When we did, she still wanted to do it, and we did. The decision was the same. The difference was that she made it from steady ground instead of from the floor.

That is the whole framework. Sort the decisions, handle the real deadlines, protect your cash and your coverage and your paperwork, and put everything else on a ninety-day hold. Do that, and the specific transition you are facing becomes a series of manageable steps instead of one overwhelming wall.

The rest of this paper walks through the transitions where I see people most often, and what the specific pieces look like inside each one.

Career Transition and Corporate Restructuring

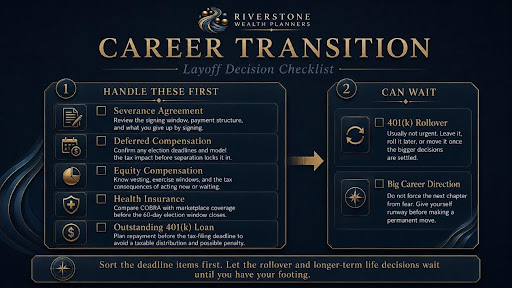

This is the transition I am seeing most right now. Companies restructure, divisions get consolidated, and capable people at the mid and senior levels find themselves holding a severance agreement they have thirty or forty-five days to sign. If that is you, the first thing to know is that a layoff at your level is rarely a simple "here is your last paycheck" event. There are usually several financial decisions bundled into it, some with real deadlines, and the quality of the choices you make in the first sixty days can matter for years.

Here is how the pieces sort out.

The severance agreement itself. You have a signing window, and that window is a real deadline, so this goes in the first bucket. But a deadline to sign is not a reason to sign immediately. Read what you are actually being offered. Severance is often negotiable, especially at senior levels, and the number on the first draft is frequently not the final number. Understand how it is paid, because lump-sum versus salary-continuation has real tax and cash-flow consequences, and understand what you are giving up by signing, which is usually your right to bring certain claims later. This is a document worth having a professional set of eyes on before you sign, not after.

Deferred compensation. If you participated in a nonqualified deferred comp plan, separation can trigger distribution elections that are locked the day you leave, and getting this wrong is expensive and permanent. Some plans pay out on a schedule you chose years ago. Some force a lump sum on separation, which can land a large taxable event in a single year, in the same year your regular income also changes. This belongs in the deadline bucket, and it is one of the pieces people most often overlook because it is not front-of-mind the way the severance check is.

Equity compensation. RSUs, ISOs, NSOs, and any stock you hold all have their own clocks when you leave. Vested equity may need to be exercised within a set window after separation, often ninety days for options, and that window does not care about your other crises. Unvested equity is usually forfeited, though sometimes severance negotiations can accelerate a portion. The tax treatment of exercising options in a year when your income has changed is worth modeling before you act, because the interaction between an option exercise and a lower-income year can be either a trap or an opportunity depending on how it is sequenced.

Health insurance. When employer coverage ends, you have a COBRA election with a 60-day window, and you have the marketplace as an alternative. COBRA keeps your existing plan but you now pay the full premium yourself, which is often a shock. The marketplace may be cheaper, and if your income for the year is going to be lower than usual, you may qualify for subsidies you would not normally see. This is a real decision with a real deadline, not an automatic default to COBRA.

The 401(k). This one is almost never urgent, which is exactly why it belongs in the "can wait" bucket even though it feels like it should be handled immediately. Your 401(k) does not evaporate when you leave. You generally have four options: leave it where it is, roll it to an IRA, roll it to a new employer's plan, or cash it out, and cashing it out is almost always the wrong answer. There is rarely any reason to rush this decision in the first thirty days. One nuance worth flagging, because it is genuinely valuable and often missed: if you hold highly appreciated company stock inside the 401(k), a strategy called net unrealized appreciation may let you treat the gain as long-term capital gains instead of ordinary income. That one is worth a conversation before you roll anything, because rolling first can close the door on it.

An outstanding 401(k) loan. If you borrowed against your 401(k) and still owe a balance when you leave, the rules change the moment you separate, and this one moves straight into the deadline bucket. While you were employed, you repaid the loan through payroll deductions on a comfortable schedule. Once you are gone, that schedule usually accelerates hard. You typically have until the tax filing deadline for the year you left, including extensions, to repay the balance or roll it into an IRA. Miss that window and the outstanding balance is treated as a distribution. That means it becomes taxable income for the year, and if you are under 59½, it usually carries an additional 10 percent early withdrawal penalty on top. So a loan you were quietly paying off can turn into a surprise tax bill in the same year your income already changed, which is the worst possible timing. If you have an outstanding 401(k) loan, this is one of the very first things to put on the list, not something to discover in April.

Put those together and the shape of the first sixty days becomes clear. Sort the deadline items, the severance window, the deferred comp election, the equity exercise window, the loan repayment clock, and the COBRA deadline, and handle those first. Let the 401(k) rollover and the longer-term "what do I do now" questions wait until you have your footing. And keep the biggest decision of all, which is often "should I take another job like the last one or change direction entirely," in the third bucket. That is a life decision wearing a financial costume, and it should not be made in the first month from a place of fear.

The people who navigate a restructuring well are not the ones who scramble to replace the income by Monday. They are the ones who bought themselves a runway, handled the time-sensitive money decisions cleanly, and gave themselves room to make the big choice from steady ground.

Before the Announcement

Not everyone reading this has already been laid off. Some of you are watching it come. The division is underperforming, the reorganization talk has started, the meetings have a different tone, and you are fairly sure your seat is one of the ones at risk. You have not gotten the news, but you can feel it.

I have been in that position myself, under the shadow of it for a long stretch without knowing which way it would break, so I want to speak directly to the person sitting in that particular kind of dread.

The best time to prepare for a job loss is while you still have the job. Every financial move is easier from inside the building than outside it. Build your cash runway now, while the paychecks are still landing, because money you set aside while employed is worth far more than money you scramble for after. Take care of any health needs while your coverage is still active and cheap. Understand your equity and deferred compensation vesting schedule before anyone forces the timing, so you know exactly what you would be walking away from and whether a vesting date worth waiting for is close. Hold off on any large new financial commitment, the bigger mortgage, the major purchase, until you know where you stand. None of this is dramatic. All of it puts you on higher ground before the water rises.

There is one assumption worth challenging while you still have time to plan around it. Almost everyone underestimates how long the gap will last. The mental math tends to be optimistic, a month or two, three at the outside, and then the search takes longer than expected, especially at senior levels where the right seat is rarer and the hiring process is slower. A search that runs six or nine months is common, not catastrophic. If you build your runway assuming a short gap and the gap runs long, the pressure to take the first offer that comes along, whether or not it is the right one, gets intense at exactly the wrong moment. Plan for the longer timeline. If it resolves faster, you have lost nothing. If it runs long, you have protected yourself from making a rushed decision out of financial fear.

The other piece is what you do with the anxiety itself. Dread feeds on stillness. The people I have seen come through this waiting period in the best shape are the ones who put the worry to work instead of pacing with it. That might mean sharpening a skill, rebuilding a network that has gone quiet, earning a credential that makes you harder to let go and more valuable if you do leave, or starting the thing you have been putting off. The specific move is yours to pick. The principle is that forward motion is the antidote. Doing something, ideally something that both strengthens your position and gives the worry somewhere productive to go, beats sitting still and waiting for something to happen to you.

If you are in that waiting place right now, use the time. It is the one advantage the still-employed have over the already-departed, and it disappears the day the announcement comes.

Divorce

Divorce is a financial transition wearing an emotional disguise, and the two get tangled worse here than almost anywhere else. It is a legal process, a financial restructuring, and one of the hardest personal experiences a person goes through, all happening at once and on a timeline someone else often controls. The three-bucket framework matters here more than ever, because the emotional pull to make permanent decisions from a place of hurt or anger is strongest exactly when the stakes are highest.

I want to walk through this in two parts, because divorce has a during and an after, and the financial work is different in each.

During: the process itself. While the divorce is in motion, most of the big financial decisions are being negotiated, not made unilaterally, which means the goal is to go in informed rather than to act fast. A few things are worth understanding before you are at the table.

Not all assets that look equal are equal. A retirement account and a brokerage account of the same dollar value are not worth the same after taxes, because one is taxed on the way out and one may already have embedded gains. The house is rarely the prize it feels like, because it comes with a mortgage, maintenance, taxes, and the question of whether you can carry it on one income. None of this is about winning. It is about understanding what you are actually agreeing to, because a settlement that looks fair on the surface can be quietly lopsided once taxes and carrying costs are accounted for.

A closer look at the QDRO. If a workplace retirement plan is being divided, a 401(k), a 403(b), or a pension, it takes a specific court order called a Qualified Domestic Relations Order, and there are a few things about it that catch people off guard.

The first is that the divorce decree by itself does not move the money. A settlement saying you are entitled to half of a retirement account is not the same as actually receiving it. The QDRO is a separate document that has to be drafted, signed by the court, and then accepted by the plan administrator, who has their own rules about what the order must say. Until all of that happens, nothing moves. This is the step that most often gets left until the end and sometimes gets forgotten entirely, and a QDRO that never gets filed is one of the quiet disasters in divorce. Years later the participant retires, remarries, or passes away, and the money that was supposed to be split is tangled up or gone. Get the order drafted and accepted while everyone is still cooperating and the paperwork is fresh.

The second is that a QDRO is for employer plans only. IRAs are not divided this way. An IRA is split through language in the divorce agreement itself, handled as a transfer between the two IRAs, and this distinction matters more than it sounds. If you pull money out of an IRA to hand to an ex-spouse without doing it as a proper transfer, you can create a taxable event and a penalty on money that was only ever meant to change hands. The mechanics are different for the two account types, and using the wrong one is an expensive mistake.

The third is a genuine opportunity that is easy to miss. If you are the spouse receiving retirement money through a QDRO and you actually need some of it as cash, there is a narrow window where you can take a distribution directly from the employer plan without the 10 percent early withdrawal penalty, even if you are under 59½. You still owe ordinary income tax on it, but the penalty is waived. The catch is that this only works at the plan level, before the money is rolled into an IRA. The moment it lands in your own IRA, that window closes, and any early withdrawal after that gets hit with the penalty like normal. So if you know you will need a chunk of the settlement in cash, the sequencing matters. Take what you need out of the plan first, then roll the rest. Roll everything first and you have given up the exception.

And for pensions specifically, dividing one is its own conversation. The order has to spell out how the benefit is split and what happens to survivor benefits, and the choices made in that document affect what you actually receive years down the road. This is not a form to fill out casually. It is worth having someone who does this work regularly involved before it is finalized.

Two numbers get overlooked in almost every divorce I have seen, and both of them can quietly reshape your life after the papers are signed.

The first is your actual post-divorce budget. It is easy to focus entirely on the settlement, the division of assets, who gets what, and never sit down and build the monthly picture of the life on the other side. That life usually runs on one income against fixed costs that do not shrink just because the household did. The rent or mortgage, the insurance, the car, the basic cost of living, much of it stays the same or goes up, and it is now carried by one person instead of two. A settlement can look perfectly fair on paper and still leave you underwater every month if the ongoing budget was never actually run. Build that number before you agree to anything. It tells you what you truly need out of the settlement, which is a very different question from what feels fair in the moment.

The second is your tax picture, which changes more than most people expect. Going from filing jointly to filing as a single person is not a small adjustment. The same income can land you in a higher effective tax bracket, standard deductions and thresholds shift, and financial arrangements that were tax-efficient for a married couple may not be for a single filer. It is entirely possible to come out of a divorce with what looks like adequate income and then get a genuinely unpleasant surprise the first April afterward, because the take-home on that income is lower than it was when it was taxed as part of a couple. This is worth modeling before the settlement is final, not discovering after, because understanding the real after-tax number can change what you should be negotiating for in the first place.

Both of these come down to the same principle. The settlement is not the finish line. The financial life that runs for years afterward is what actually matters, and that life is governed by two numbers, what it costs to live and what you keep after taxes, that are far too easy to leave unexamined while everyone is focused on dividing the past.

The other piece during the process is protection. Make sure you understand what accounts exist, in whose name, and what you have access to. Understand how health insurance changes, because coverage that ran through a spouse's employer ends at the divorce, and unlike a job loss, COBRA from an ex-spouse's plan has its own rules and timeline. And revisit every beneficiary designation and account title the moment the divorce is final, because the person named on your accounts and the person you now want named are almost certainly no longer the same.

After: the funds arrive. Here is the part that gets the least attention and deserves a lot of it. At some point, usually when the divorce finalizes, the financial settlement actually lands. Accounts get divided and retitled, a house gets sold or bought out, a lump sum or a series of payments begins. For many people, especially someone who was not the primary financial decision-maker in the marriage, this is the first time they are sitting on a significant pool of money that is entirely theirs to manage, and it arrives at the emotional low point of the whole ordeal.

This moment is the single most important financial decision window in the entire divorce, and it is the one people are least prepared for. The instinct is often to do something with the money immediately, to feel in control of at least this one thing after a long stretch of feeling in control of nothing. That instinct is exactly the one to resist. This is a textbook case for the third bucket. The money is not going anywhere. Park it somewhere safe, give yourself ninety days, and make the real decisions from steady ground rather than from the raw days right after the papers are signed.

What the money needs is not a fast decision. It needs a plan built around the new life, not the old one. The old financial plan was built for two people and a shared future that no longer exists. The new one has to be built from scratch, around your income, your expenses, your goals, and your timeline. That is real work, and it is worth doing deliberately. But almost none of it has to happen in the first month. The best thing you can do when the funds arrive is protect them, resist the urge to deploy them quickly, and give yourself the room to build the plan properly.

The people I have worked with who came through a divorce in the strongest financial shape were rarely the ones who fought hardest for every dollar in the settlement. They were the ones who understood what they were agreeing to during the process, and who resisted the urge to make big permanent decisions with the money the moment it landed. The divorce is the event. The financial life that follows is the thing that actually determines whether you are okay, and that one is built after the dust settles, not during the storm.

Widowhood

Of all the transitions in this paper, this is the one where the gap between what needs to happen and what a person is capable of handling is widest. You have just lost your spouse, and while you are in the earliest days of grief, a series of financial and administrative tasks lands on you, many of them with the surviving partner's name newly and solely attached. It is a great deal to ask of anyone at the worst possible time.

So this chapter is short by design. The goal in the early days is not to build a financial plan. It is to handle the few things that genuinely cannot wait, protect yourself from the decisions that should not be rushed, and give yourself permission to leave everything else for later. The three-bucket framework was practically written for this moment.

A Note on Getting Help, and Why the Long View Matters

Everything in this paper is designed to help you think clearly on your own. But the reality is that these transitions are hard to navigate alone, not because the concepts are beyond you, but because you are being asked to make clear decisions at the least clear moment of your life. That is exactly where a steady outside perspective earns its keep.

I want to be specific about what that help actually looks like, because it is not what most people assume.

The value is not in picking investments. It is in having sat in this exact chair, many times, with many people, across every one of the transitions in this paper. I have been the first call someone made the day a job ended, the day a spouse died, the day a marriage came apart, the day a business sold. And here is the part that matters most and that you cannot get from a single meeting or a one-time consultation. I did not just help those people make the decision in the moment. I stayed. I watched how the decisions played out over the years that followed.

That is the thing almost nobody talks about, and it is the whole game. Anyone can offer an opinion in the moment of crisis. What is rare, and what actually protects you, is someone who has seen how these decisions cascade. Who has watched the severance election made in year one shape the tax picture in year three. Who has seen the settlement that looked fair on paper play out across a decade of real life. Who has sat with a widow at the funeral and then again five years later and knows, from having lived it alongside her, which of the early decisions she was glad she made slowly and which of the rushed ones she wished she had back.

You only get that from time. From being there at the inception of the decision and staying through the years of consequences that follow. That accumulated experience, across many people and many transitions and many years, is the actual product. It is why people hire us, and it is worth far more than any single number on an investment statement.

Investment performance matters, and we take it seriously. But if you think that is the whole job, you have been sold a thin version of what an advisor is for. The real work is being a steady presence through the moments that reshape a life, someone who has seen this movie before and can tell you, from experience rather than theory, which decisions deserve your fear and which ones do not. In the moment of a transition, that is worth more than almost anything else.

If any of this resonates, and you are facing one of these moments now or can see one coming, that is exactly the kind of conversation we are built for. You can see what it actually looks like to work with us, and what it means to have someone in that seat alongside you, here: What the First Year Working Together Actually Looks Like.

And if you take nothing else from this paper, take this. Almost nothing has to be decided today. Protect what needs protecting, refuse the permanent decisions until you are steady, and give yourself the room to make the important choices from solid ground. Whatever you are walking through, it is survivable, and you do not have to navigate it alone.