Why Your Accounts Being Scattered Is Costing You More Than You Think

When new clients come to Riverstone Wealth Planners for the first time, one of the most common things we discover during the initial planning process isn't a bad investment or a poorly designed portfolio. It's that nobody has actually looked at the full picture in years.

Accounts at three different institutions. An old 401k from a job they left in 2019. A brokerage account opened during the pandemic. A Roth IRA somewhere. Cash sitting in a checking account earning nothing because it built up and nobody got around to deploying it. A concentrated position in employer stock that grew quietly while nobody was watching. A business that became the largest asset on the balance sheet but exists entirely outside any investment strategy.

Individually, each of these is understandable. Together, they represent a financial life that has accumulated rather than been managed.

This post is written for the clients we work with most often. Pharma and life sciences executives in New Jersey who are too busy with demanding careers to actively manage their accounts. Business owners whose net worth is dominated by the business they built but whose investable assets sit unattended. Independent women navigating divorce, widowhood, or inheritance who may have been kept in the dark on investment matters for years and are now trying to take control. Each situation looks different on the surface but the underlying problem is the same.

The Hidden Cost of Disorganization

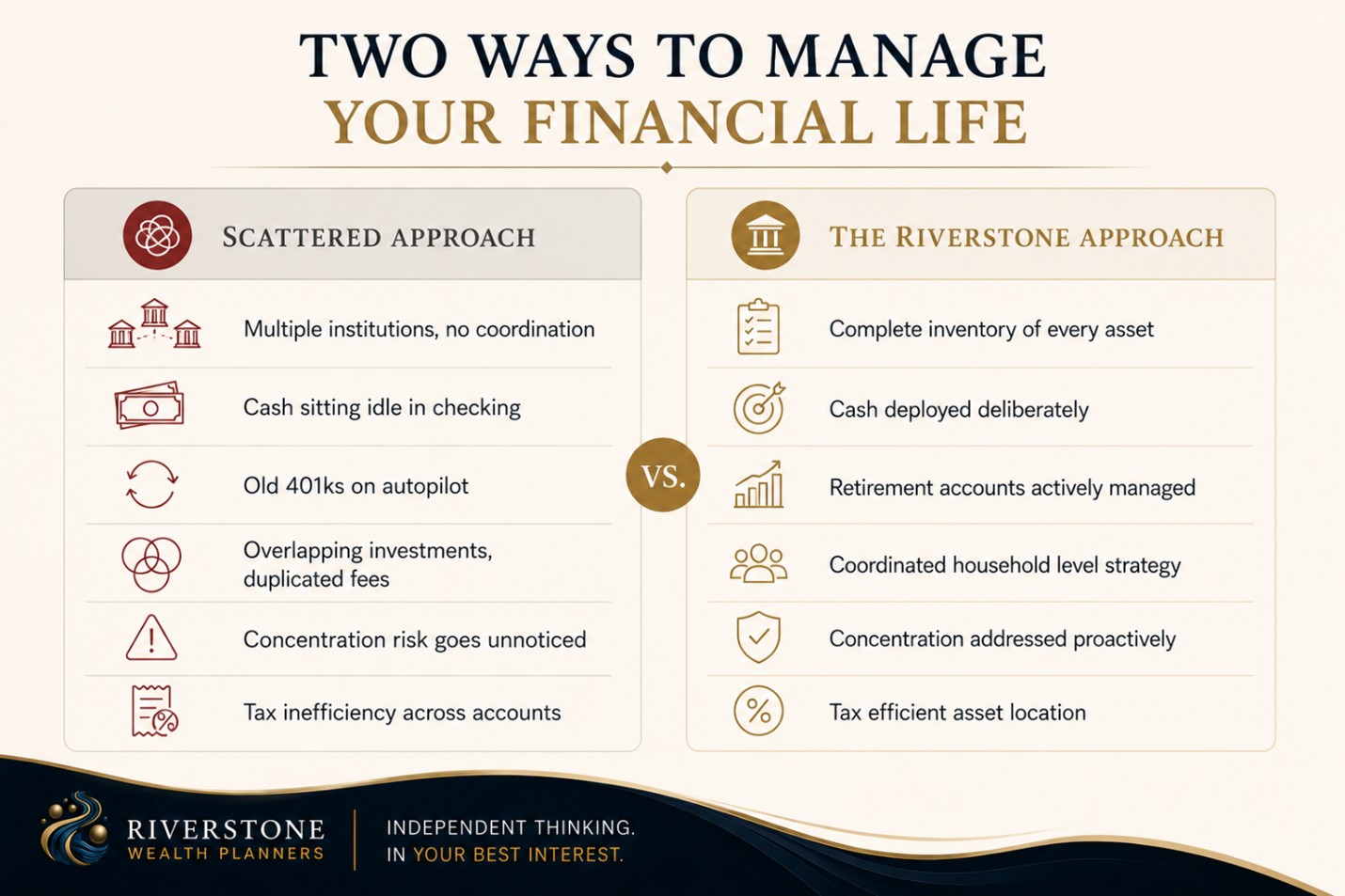

Most people underestimate the cost of having their financial life scattered across multiple institutions and accounts. The actual cost shows up in five distinct ways.

Cash that isn't working. Almost every new client we onboard has too much cash sitting in checking and savings accounts, sometimes far more than they need for any reasonable emergency fund or short term spending. That cash is losing purchasing power every year to inflation. In a market where short term Treasury yields are meaningful, the opportunity cost is significant.

Old retirement accounts on autopilot. The 401k from your previous employer is probably still invested in whatever you selected the day you enrolled. The target date fund chosen for an age you no longer are. The fund lineup that's been quietly underperforming for years. Nobody is watching it because it's not at your current employer and not at your current advisor's firm.

Overlapping investments without coordination. When accounts exist at multiple institutions, you often own the same investments in multiple places without realizing it. That creates concentration risk you didn't intend, duplicates fees, and prevents the kind of coordinated rebalancing that real portfolio management requires.

Tax inefficiency across accounts. Different account types have different tax characteristics. The same investment held in a 401k versus a taxable account versus a Roth IRA generates dramatically different after tax outcomes. Without someone looking at all of it together, the wrong investments end up in the wrong accounts and the long term cost compounds.

Concentration risk that goes unaddressed. Pharma executives often have 30 to 50% of their net worth in company stock without realizing how concentrated they've become. Business owners often have 70% or more of their net worth tied to the business itself. When nobody is mapping the full balance sheet, these exposures grow quietly and create real risk.

What This Looks Like for Each of Our Clients

The scattered account problem looks different for each of our three primary client groups, but the underlying issue is the same.

For pharma executives, the most common pattern is multiple old 401ks from previous employers, a current 401k that's being contributed to but not actively managed, RSUs and exercised options sitting in a brokerage account at the company stock plan administrator, a Roth IRA somewhere from earlier in their career, and a checking account with significantly more cash than needed. Add concentrated company stock to the mix and the result is a balance sheet that nobody has ever actually mapped.

For business owners, the pattern is similar except the business itself often represents the largest single asset. The investable portion of their net worth gets neglected because all the attention goes to the business. Cash builds up. Retirement contributions happen but don't get optimized. The eventual liquidity event creates a sudden complexity that nobody planned for because the investable assets had always been a secondary concern.

For independent women navigating major transitions, the pattern is often more dramatic. A divorce or widowhood suddenly puts them in charge of assets they may have had limited visibility into for years. The accounts they inherited or received in settlement are at institutions chosen by someone else, invested in strategies they didn't choose, and require active management decisions they weren't prepared for. The first step is simply understanding what they have.

It Starts With a Financial Plan

Every new client relationship at Riverstone begins with a comprehensive financial plan. This is intentional, and it's the most important step in solving the scattered account problem.

The financial planning process is what brings the full picture into focus. Before we invest any of your money, before we make any recommendations about consolidation, before we touch a single account, we build a customized financial plan that captures every asset you own, every account you have open, how each account is currently invested, and the tax characteristics of each.

I have built hundreds of financial plans over nearly two decades of practice. And I have seen firsthand the clarity this process creates when clients finally have a real understanding of not only what they own, but where it is, how it's invested, and how it all fits together.

For many years now, clients have come to me asking the same questions. What do I do with all the cash I have sitting at the bank? What should I do with my company stock? What about all the equity compensation I keep accumulating? How does my business factor into my retirement plan? The financial planning process is how those questions get answered, not in isolation, but in the context of the full picture.

By the time you see your finished plan, you'll know exactly what you own, what it's worth, how it's currently invested, what taxes apply to each piece, and what we recommend going forward. The clarity that creates is often the single biggest immediate value new clients experience when they come to work with us. It transforms a financial life that has felt overwhelming or unclear into something that finally makes sense, with a defined path forward.

How We Bring Everything Into Focus

The process of bringing a scattered financial life into focus follows a consistent pattern.

We start with a complete inventory. Every account, every position, every cash balance, every outside asset. The first time a new client sees everything mapped in one place is often the first time anyone in their financial life has done this for them.

From there we identify the immediate issues. Cash that should be working. Old 401ks that should be consolidated or rolled over. Overlapping positions that need to be cleaned up. Concentrated exposures that need to be addressed.

We build a coordinated strategy across all accounts. Asset location decisions about which investments belong in which accounts. Rebalancing happens at the household level rather than the individual account level. Tax planning becomes possible because we can see the full picture.

We consolidate where it makes sense. Sometimes the right move is to bring assets to LPL where we can manage them directly. Sometimes accounts make sense to leave where they are if there are tax or planning reasons. The point is that the decision is made deliberately rather than by default.

We stay engaged ongoing. Once the picture is clear, keeping it clear requires ongoing attention. Annual reviews. Quarterly check ins. Active monitoring of cash levels, concentration positions, and outside accounts that need to remain coordinated.

Common Questions About Account Consolidation

Do I have to move all my accounts to work with you?

No. The goal is coordination, not consolidation for its own sake. Sometimes the right answer is to move accounts under our management. Sometimes accounts make sense to leave at their current institution. We make these decisions based on what's actually best for you, not based on what increases assets under our management.

What happens to my old 401k from my previous employer?

There are typically four options. You can leave it at the former employer if their plan is good and the investment options are strong. You can roll it into your current employer's 401k if that plan accepts rollovers. You can roll it into a traditional IRA where it has access to a broader investment universe. Or in some cases you can convert it to a Roth IRA, though that creates a tax event. The right answer depends on your specific situation. We walk through the options with you so you can make an informed decision.

I'm a pharma executive with concentrated company stock. How do you handle that?

Concentrated company stock requires a thoughtful approach because of the tax implications of diversifying. We typically build a multi year diversification plan that reduces exposure gradually, coordinates with tax planning to minimize the impact, and often uses tools like donor advised funds or exchange funds to manage the transition tax efficiently. The goal is to reduce risk over time without triggering an avoidable tax bill.

I'm a business owner. How does my business factor into the overall financial picture?

The business is a major asset that needs to be considered alongside investable assets even though it isn't managed in the same way. We model what a potential business sale would look like, what the liquidity event would mean for your overall balance sheet, and how to think about diversification of the investable assets in the meantime. The business shapes everything else about the financial plan.

I went through a divorce and have assets I need to manage but I don't know where to start.

This is one of the most common situations we work with. The first step is always understanding what you have. We help you inventory every account, every asset, every income source. From there we build a plan that's appropriate for your new situation rather than continuing whatever strategy was in place before. There's no judgment about how much or how little you knew before. The point is getting you to a place where you understand and control your financial life going forward.

How much cash should I actually be holding?

The right amount of cash depends on your situation, but most of our new clients are holding significantly more than they need. A reasonable emergency fund is typically three to six months of essential expenses, sometimes more for business owners with variable income. Beyond that, cash that isn't earmarked for a near term goal is usually better deployed into investments. We help you figure out the right number for your situation.

Do you charge to consolidate accounts?

No. The consolidation work is part of the onboarding process and the ongoing relationship, not a separate charge. Our fee structure is based on assets under management or planning engagement, depending on the relationship. The actual work of bringing accounts into focus is included.

What This Means in Practice

The clients who get the most out of working with Riverstone are the ones who let us help them bring order to a financial life that has accumulated rather than been managed. The relief that comes from finally seeing everything in one place is often the first emotional shift new clients experience. The financial benefits follow from there.

Cash starts working. Old accounts get optimized or consolidated. Concentration risk gets addressed deliberately. Tax planning becomes possible because we can see everything. The portfolio gets built around the full picture instead of just the assets that happen to be in front of us.

If your financial life feels scattered, or if you've been telling yourself you should really get around to looking at that old 401k for the past several years, reach out directly. The first conversation is straightforward and there's no obligation beyond it.

Bill Clinton, CFP®, CIMA®, CPWA®Riverstone Wealth Planners Chester, NJ 908-888-6906

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.