The Widow's Tax Penalty: A Planning Challenge Nobody Talks About Enough

Part of the Riverstone Tax Planning Series

Of all the tax planning conversations I have with clients, this one might be the most important and the least discussed.

It doesn't have an official name in the tax code. Financial professionals call it the Widow's Tax Penalty, or sometimes the Widow's Tax Trap. Whatever you call it, the impact is real, it affects a significant number of people, and in most cases it's entirely plannable if you know it's coming.

A meaningful portion of the clients I work with here in Morris County and throughout northern New Jersey are independent women, some of whom are widows or going through the transition of losing a spouse. It's one of the most financially complex and emotionally overwhelming periods a person can navigate. The last thing anyone needs in that moment is a surprise tax bill that nobody warned them about.

This article is about making sure you're not caught off guard.

What the Widow's Tax Penalty actually is

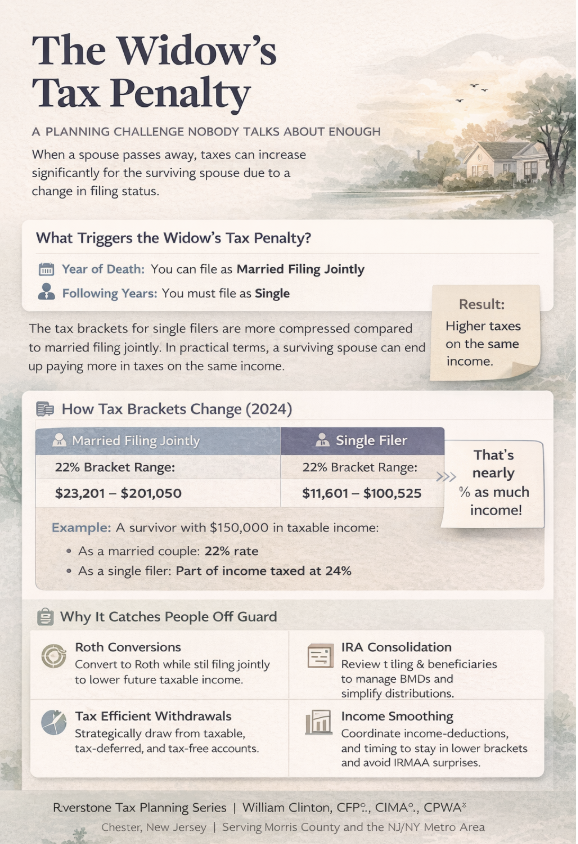

When a spouse passes away, the surviving spouse can file as "married filing jointly" for the tax year in which the death occurred. Starting the following year, however, they must file as a single taxpayer.

That shift sounds administrative. The financial consequences are anything but.

The tax brackets for single filers are significantly compressed compared to married filing jointly. In practical terms, a surviving spouse can end up paying taxes at a higher rate on the exact same income, simply because of how their filing status changed. They didn't earn more money. Their circumstances didn't improve. Their tax bill went up anyway.

Here's a simple way to think about it. In 2024, the 22% tax bracket for married filing jointly applied to taxable income up to roughly $201,050. For a single filer, that same 22% bracket topped out at about $100,525. Cut nearly in half. So a widow with $150,000 in taxable income who was previously in the 22% bracket may now find a portion of that income taxed at 24%.

Multiply that difference across a retirement that could last 20 or 30 years and the cumulative impact becomes very significant.

Why it catches people off guard

The Widow's Tax Penalty tends to hit hardest when it combines with other income sources that don't automatically adjust downward when a spouse passes.

Required Minimum Distributions are a good example. If a couple had two IRAs, the surviving spouse now has a single IRA, but often inherits the deceased spouse's IRA as well. The total balance subject to RMDs may not change dramatically, but all of that income is now being reported on a single return with compressed brackets.

Social Security adds another layer. When a spouse passes, the surviving spouse typically keeps the higher of the two Social Security benefits and loses the lower one. That's the right outcome, but it also means Social Security income doesn't drop by as much as you might expect. Combined with RMDs and any pension income, a surviving spouse can find themselves with more taxable income than anticipated at a higher effective rate than they've ever paid before.

Medicare premiums compound the issue further. As I covered earlier in this series, IRMAA surcharges are triggered by income levels, and the thresholds for single filers are lower than for married couples. A surviving spouse whose income doesn't change dramatically may still find themselves crossing an IRMAA threshold simply because the filing status changed.

The emotional dimension matters here

I want to be direct about something that doesn't always come up in financial planning articles.

The year or two following the loss of a spouse is not the time when most people are thinking clearly about tax optimization. Grief is real, and it affects decision-making in ways that are completely understandable. Financial decisions that seem manageable under normal circumstances can feel overwhelming when someone is also processing loss, managing an estate, potentially relocating, and restructuring their entire life.

This is exactly why I believe planning for this scenario needs to happen before it becomes urgent. For married couples, the Widow's Tax Penalty is a knowable, plannable event. We can look at current account balances, projected RMDs, Social Security benefits, and income sources and model what the tax picture looks like for a surviving spouse. That analysis is not morbid. It's protective.

For the independent women I work with throughout Morris County and the New Jersey area, many of whom have already navigated this transition, the planning conversation often shifts from prevention to management. The question becomes: given where things are now, what can we do to reduce the ongoing tax impact going forward?

The answer is usually some combination of the strategies I'll outline below.

What thoughtful planning looks like

There is no single solution to the Widow's Tax Penalty, and anyone who tells you there is isn't giving you the full picture. The right approach depends heavily on income sources, account structures, estate considerations, and timing. But there are several planning levers worth understanding.

Roth conversions before the filing status changes. As I discussed in the prior article in this series, Roth conversions are most valuable when done during lower-income years. For married couples, the years before one spouse passes, when filing jointly still applies, may offer a window to convert traditional IRA assets to Roth at lower rates. Every dollar shifted to a Roth account is a dollar that won't generate taxable income for a surviving spouse later.

IRA consolidation and beneficiary planning. How IRAs are titled and who is named as beneficiary has real consequences for a surviving spouse. Making sure these designations are current and intentional is one of the most basic but impactful things a couple can do before either spouse passes.

Coordinating Social Security timing. The decision about when to claim Social Security, particularly for the higher earner in a couple, has long-term implications for a surviving spouse. Delaying the higher benefit increases the amount the survivor will receive. That's generally positive, but it also means more income subject to the compressed single-filer brackets. Understanding that tradeoff in advance allows for better planning around other income sources.

Qualified Charitable Distributions for surviving spouses who give to charity. As I covered earlier in this series, QCDs allow individuals 70½ or older to transfer IRA funds directly to charity, satisfying RMD requirements without adding to taxable income. For a surviving spouse managing a higher-than-expected tax burden, this strategy can be particularly valuable.

Managing the transition year carefully. The year of a spouse's passing is often the last year of married filing jointly status. That year can sometimes be used strategically, for example, to do a larger Roth conversion at the still-favorable joint rates before the filing status changes. This requires working with both a financial advisor and a tax professional, but the opportunity is real.

Planning for independent women in Morris County and Northern New Jersey

A significant portion of my practice here at Riverstone Wealth Planners in Chester, New Jersey involves working with independent women, including widows and women navigating major financial transitions. These conversations are among the most important I have, and they require both technical depth and genuine sensitivity to what someone is actually going through.

If you are a widow, or if you and your spouse have not yet had a conversation about what the financial picture looks like for the surviving partner, I'd encourage you to have that conversation sooner rather than later. Not because it's comfortable, but because the planning options available before this transition are considerably broader than the ones available after.

Riverstone Wealth Planners serves clients throughout Morris County, Chester, Mendham, Far Hills, Bernardsville, and the broader NJ/NY metro area. We also work with clients nationally through a fully virtual planning experience.

Frequently Asked Questions

What is the Widow's Tax Penalty? The Widow's Tax Penalty refers to the higher tax burden a surviving spouse often faces after the death of a partner. Because they must file as a single taxpayer starting the year after the death, their income is subject to compressed tax brackets, which can result in a higher effective tax rate on the same income they had as a married couple.

How much can the Widow's Tax Penalty increase taxes? The impact varies depending on income and account structure, but it can be substantial. Tax brackets for single filers are roughly half the width of those for married filing jointly, which means income that was previously taxed at 22% may be partially taxed at 24% or higher after a filing status change.

Can the Widow's Tax Penalty be avoided? It can't be eliminated entirely, but it can be meaningfully reduced with advance planning. Strategies like Roth conversions, careful Social Security timing, Qualified Charitable Distributions, and coordinated withdrawal planning can all help reduce the ongoing tax impact for a surviving spouse.

When should couples start planning for this? The earlier the better, ideally well before either spouse's health becomes a concern. The planning options available while both spouses are healthy and income is predictable are considerably broader than those available in the immediate aftermath of a loss.

Where can I find a financial advisor in Morris County NJ who works with widows and independent women? Riverstone Wealth Planners, based in Chester, New Jersey, works with independent women and widows throughout Morris County and northern New Jersey on retirement income planning, tax strategy, and financial transitions. You can schedule a complimentary conversation at the link above.

William Clinton, CFP®, CIMA®, CPWA® | Riverstone Wealth Planners Chester, New Jersey | Serving Morris County and the NJ/NY Metro Area

This material is for informational purposes only and should not be considered individualized financial, tax, or legal advice. Individuals should consult with a qualified financial professional, tax advisor, or attorney regarding their specific situation. Advisory services are offered through Riverstone Wealth Planners. Securities and advisory services may be offered through LPL Financial, a registered investment advisor and member FINRA/SIPC. Tax laws are subject to change, and the impact of any strategy will vary based on individual circumstances.