The Hidden Tax Risks of Large IRA Balances in Retirement

Part of the Riverstone Tax Planning Series

I want to tell you something that surprises almost every client I share it with.

That large IRA balance you've spent decades building? The IRS has a claim on every single dollar of it. And starting in your early 70s, they get to decide how much you hand over each year, whether you need the money or not.

Most people understand, in a general sense, that traditional IRA withdrawals are taxed. What they underestimate is how that tax exposure compounds over time, quietly, persistently, and in ways that can fundamentally reshape what retirement actually looks like.

This article is about that problem. More importantly, it's about what you can do about it.

The account that looks bigger than it is

When a client comes in with a $1.2 million IRA, I don't see $1.2 million. I see $1.2 million minus whatever federal and state taxes will apply when that money is eventually withdrawn. Depending on the client's situation, that could be 22%, 24%, or higher. Which means the real, spendable value of that account is meaningfully less than what the statement shows.

This isn't a technicality. It's a planning reality that shapes every conversation I have about retirement income.

Traditional IRAs and 401(k)s are funded with pre-tax dollars. The deal you made with the IRS when you contributed was simple: defer the tax now, pay it later. For decades, that tradeoff works in your favor. Your money grows without being eroded by annual taxes. But "later" eventually arrives. And when it does, every dollar you withdraw is taxed as ordinary income. Not at capital gains rates. Ordinary income, the same rate structure that applied to your paycheck when you were working.

For clients with large balances, this creates a gap between the number they see on paper and the income they can actually spend. Understanding that gap clearly is one of the most valuable things we can work through together.

When the IRS starts making decisions for you

Here's where the situation gets more complicated.

Once you reach age 73, the IRS requires you to begin taking minimum withdrawals from your traditional retirement accounts each year. These are called Required Minimum Distributions, or RMDs, and they are not optional. The amount is calculated based on your account balance and a life expectancy factor set by the IRS. It increases each year. And it doesn't care whether you need the income, whether the market is up or down, or whether the withdrawal pushes you into a higher tax bracket.

For clients with large IRA balances, RMDs can be significant. I've worked with clients whose RMDs alone generate more taxable income than they ever spent in a year during their working lives. That's not an exaggeration. It's a direct consequence of decades of disciplined saving without a coordinated withdrawal strategy to match.

The tax impact compounds in a straightforward but often overlooked way: a larger balance generates a larger RMD. A larger RMD means higher taxable income. Higher taxable income can push you into a higher bracket and trigger consequences beyond just your tax bill.

The Medicare problem most people don't see coming

One of the most frustrating conversations I have with clients is explaining why their Medicare premiums just increased significantly.

Medicare premiums are not flat. They're income-sensitive. Through a mechanism called IRMAA (Income-Related Monthly Adjustment Amounts), higher income in retirement triggers higher premiums. And the income figure the government uses is your Modified Adjusted Gross Income from two years prior. So a large RMD, or an unplanned income spike, can result in meaningfully higher Medicare costs before you even realize it's happening.

This is one of those planning problems that is almost entirely avoidable, but only if you're thinking about it in advance. By the time the premium notice arrives, the window to act on that year's income has already closed.

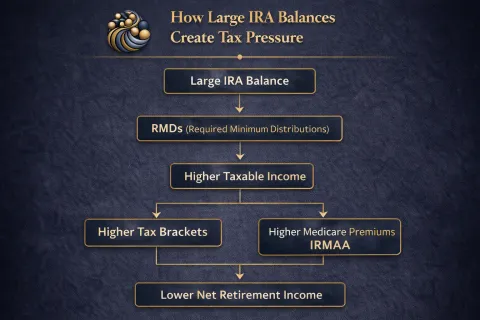

The tax compounding cycle

Put these pieces together and you can see why I describe this as a compounding problem, just compounding in the wrong direction.

A growing IRA balance leads to larger future RMDs. Larger RMDs generate more taxable income. More taxable income can push you into higher brackets and trigger higher Medicare premiums. And the income taxes paid on those distributions reduce the capital available to keep compounding inside the account.

Left unaddressed, this cycle becomes progressively harder to manage as retirement goes on. The clients who are best positioned in their 70s and 80s are almost always the ones who started thinking about this problem in their 50s and 60s, not after the RMDs had already started.

What thoughtful planning actually looks like

I want to be direct here: there is no strategy that eliminates taxes. Anyone who tells you otherwise is either mistaken or selling something. The goal is to manage when taxes occur, how much is recognized in any given year, and how your overall income is structured across the full arc of retirement.

Some of the most effective approaches I work through with clients include:

Gradual withdrawals before RMDs begin. If you retire at 62 but don't have to start RMDs until 73, that's a decade of potential planning opportunity. Drawing down the IRA gradually during lower-income years, even if you don't need the money, can reduce the balance subject to future mandatory distributions and smooth out your tax exposure over time.

Roth conversions during lower-income years. Converting a portion of a traditional IRA to a Roth account means paying taxes now, at today's rate, on money that will then grow tax-free and never be subject to RMDs. Whether this makes sense depends heavily on your current bracket, your expected future income, and your planning horizon. It's not right for everyone, but for clients in the right situation, it can be one of the highest-impact moves available.

Qualified Charitable Distributions for clients who give to charity. If you're 70½ or older and charitably inclined, there's a strategy worth knowing about. A Qualified Charitable Distribution (QCD) allows you to transfer money directly from your IRA to a qualified charity. The transfer can count toward your RMD for the year, and the amount is not included in your taxable income. For a client who was planning to donate anyway, this is simply a more tax-efficient way to do it, and it can meaningfully reduce the income that drives both your tax bracket and your Medicare premiums.

The bottom line

A large IRA is a genuine achievement. Decades of saving, compounding, and discipline built it. But without a coordinated plan for how that money comes out, a meaningful portion of what you built will go to taxes in ways that could have been managed differently.

The clients I work with who navigate this best share one thing in common: they started the conversation early. Not the year before RMDs began, but years before, when there was still time to shape the outcome.

If you'd like to sit down and look at how your current retirement accounts may affect your tax picture in retirement, and what options might be worth considering, I'd welcome the conversation. Click Here to Schedule a call!

Frequently Asked Questions

Do large IRA balances increase taxes in retirement? Yes, and often more than people expect. Every dollar withdrawn from a traditional IRA is taxed as ordinary income, and Required Minimum Distributions can force significant withdrawals regardless of whether you need the money. For clients with large balances, this can push income into higher brackets than they ever experienced while working.

What are RMDs and why do they matter? Required Minimum Distributions are mandatory annual withdrawals from traditional retirement accounts that begin at age 73. The amount increases each year and is taxed as ordinary income. For clients with large IRA balances, RMDs can significantly increase taxable income and trigger higher Medicare premiums.

What is a Qualified Charitable Distribution? A QCD allows individuals age 70½ or older to transfer funds directly from an IRA to a qualified charity. The distribution can count toward your RMD for the year and is not included in your taxable income, making it a more tax-efficient way to give for clients who are already charitably inclined.

When should I start thinking about IRA tax planning? The earlier the better, ideally in your late 50s or early 60s, before RMDs begin. That window gives you the most flexibility to evaluate strategies like gradual withdrawals, Roth conversions, and income coordination. By the time RMDs start, some options become harder to execute.

This material is for informational purposes only and should not be considered individualized financial, tax, or legal advice. Individuals should consult with a qualified financial professional, tax advisor, or attorney regarding their specific situation. Advisory services are offered through Riverstone Wealth Planners. Securities and advisory services may be offered through LPL Financial, a registered investment advisor and member FINRA/SIPC. The strategies discussed, including Roth conversions and Qualified Charitable Distributions, may not be appropriate for all individuals. Tax laws are subject to change, and the impact of these strategies will vary based on individual circumstances.