Concentration Risk: When Your Career and Your Portfolio Are the Same Bet

For most pharma executives, the single largest financial exposure isn't the stock market. It isn't interest rates. It isn't even taxes. It's the company they work for.

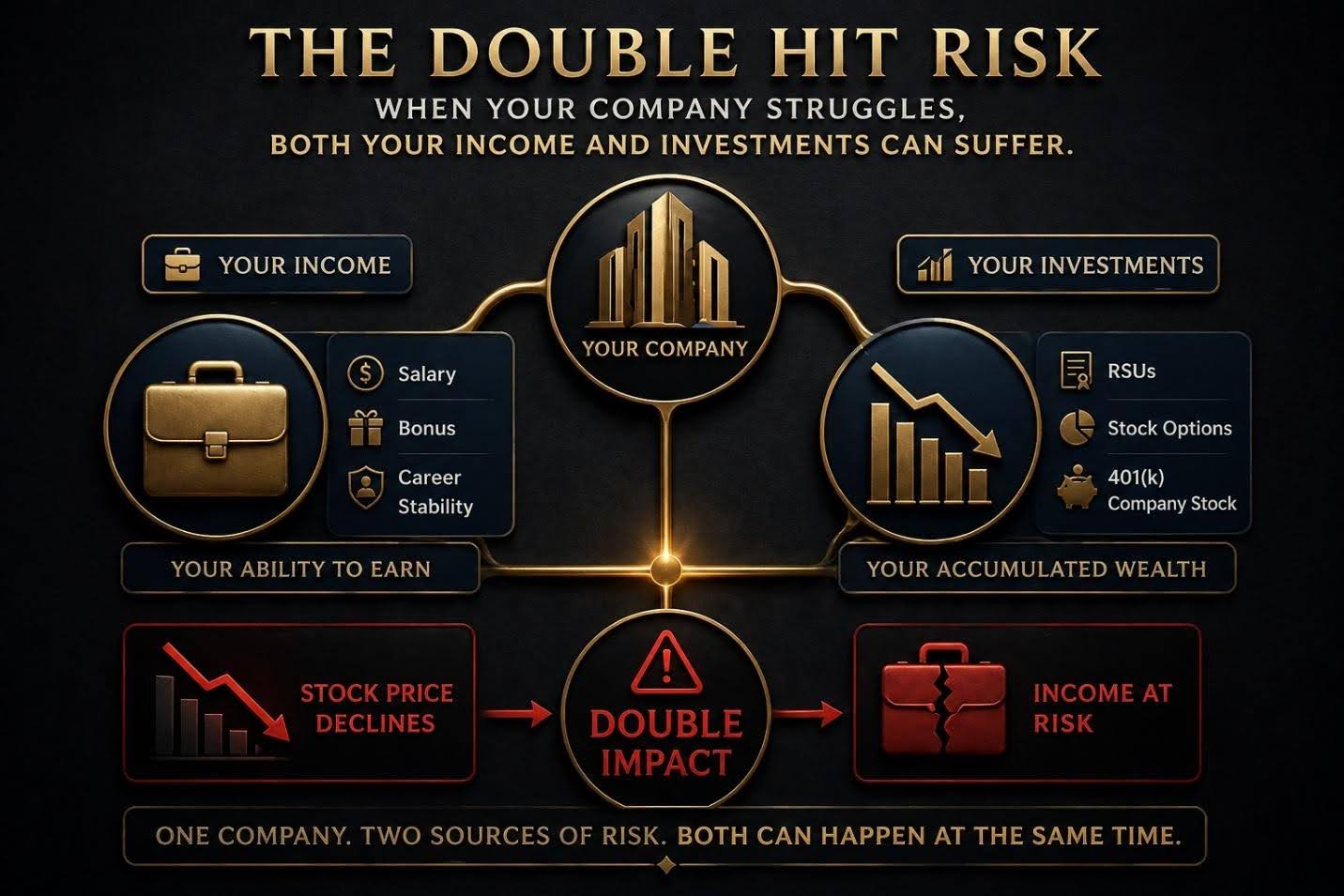

Through years of equity compensation, your wealth and your career end up tied to the same employer. RSUs vest into company stock. Options exercised result in company stock. Performance shares deliver in company stock. Deferred compensation may be tracked against company stock or other fund options. Layer on a 401(k) match potentially in company stock and an ESPP for additional accumulation, and the picture becomes clear.

Your salary depends on the company. Your bonus depends on the company. Your career trajectory depends on the company. And a meaningful percentage of your investable assets are also in the company. That's not diversification. That's a single bet, made with both your earning power and your accumulated wealth.

The Scale of the Problem

The executives I work with in Morris County and throughout northern New Jersey often have 30, 40, even 50% of their net worth tied up in the stock of a single pharma employer. In some cases the percentage is even higher. This usually isn't the result of a deliberate decision to concentrate. It's the cumulative effect of years of equity compensation that the executive never actively converted to a diversified portfolio.

The mistake isn't necessarily holding company stock. It's holding it without a plan, without an awareness of how concentrated the position has become, and without a strategy for reducing the exposure over time.

Why Concentration Risk Is Different for Executives

Concentration risk is a textbook concept in investment management. The traditional discussion focuses on portfolio risk: a single stock that drops significantly can drag down your overall returns and increase volatility.

For executives the picture is more complicated, and the risks are larger.

Your career is correlated with the same company. If your employer suffers a setback significant enough to materially affect the stock price, that same setback often affects your job. A failed clinical trial. A regulatory rejection. A merger that eliminates redundant positions. A new CEO who restructures aggressively. All of these scenarios can hit your salary, your future bonus expectations, and your investment portfolio at the same time.

That correlation is what makes executive concentration risk fundamentally different from a retail investor who happens to hold a lot of one stock. The retail investor loses money on the stock. The executive loses on the stock and their income source simultaneously.

Why Executives Resist Diversifying

Despite knowing concentration is a risk, executives often resist reducing their company stock holdings. Several reasons come up repeatedly.

There's a sense of loyalty or commitment. Selling company stock can feel like a vote of no confidence in the employer, even when there's no rational basis for that perception. Most companies don't track or care what their employees do with their vested equity, but the emotional resistance is real.

There's tax friction. Selling appreciated company stock generates capital gains, and executives often delay diversification to avoid the tax hit. This is sometimes a reasonable concern, but it can also become an excuse to avoid action indefinitely.

There's information bias. Executives often believe they understand their company better than the market does, and that belief can lead to overconfidence in the stock's prospects. Sometimes that confidence is justified. Often it isn't, especially in pharma where outcomes can hinge on factors the executive has limited visibility into.

And there's inertia. Doing nothing is easier than developing a plan. Without a forcing function, most executives let their concentrated positions grow indefinitely.

What Experience Has Taught Me

A few things have become clear from working on these decisions with executives over the years.

First, the right approach to concentration is gradual, not all at once. Selling 100% of your company stock immediately is rarely the right answer because it triggers significant tax exposure and ignores the fact that the position may continue to perform well. A multi year diversification plan that sells a defined percentage on a scheduled basis spreads the tax impact and removes the emotional decision making from each individual sale.

Second, the timing of diversification can be coordinated with other tax planning. A year with significant capital losses elsewhere in the portfolio creates an opportunity to harvest gains on company stock at low or zero net tax cost. A year with charitable giving plans can use appreciated company stock as the funding source, eliminating capital gains while generating a deduction.

Third, this work is done in partnership, not in isolation. For every client with concentrated equity exposure, we coordinate with your CPA on timing and tax impact. We also coordinate with your estate planning attorney when concentrated positions are part of broader wealth transfer planning. The right strategy isn't just about reducing exposure. It's about reducing exposure efficiently across all the tools available.

Fourth, concentration risk is something to address before it becomes a crisis, not after. The executives who experience the worst outcomes are the ones who waited until something went wrong with the company to start thinking about diversification. By then the stock has often already declined and the planning options have narrowed.

Common Questions About Concentration Risk

How concentrated is too concentrated?

There's no universal answer, but most planning frameworks suggest that any single stock representing more than 10 to 15% of your investable net worth deserves active management. For executives whose career income also depends on the same company, the threshold is often lower because the correlation between portfolio risk and career risk amplifies the exposure.

Should I sell all my company stock?

Almost certainly not all at once, and probably not all eventually either. Many executives reasonably hold a meaningful position in their employer's stock. The question is whether the position is the result of a deliberate decision or the result of accumulated drift, and whether you have a plan for managing it over time.

What about 10b5-1 plans?

A 10b5-1 plan is a pre-set selling schedule that allows executives to sell company stock on a defined cadence regardless of what's happening at the company. These plans are particularly useful for executives who have access to material non public information and want to be able to sell legally and consistently. They also remove the emotional decision making from each sale, which is often the biggest barrier to executing a diversification strategy.

What about exchange funds?

Exchange funds are pooled investment vehicles that allow executives to contribute concentrated stock and receive diversified shares in return without triggering immediate capital gains. They have specific rules including a seven year holding period, and they're not appropriate for everyone, but they can be a useful tool for executives with very large concentrated positions and high embedded gains.

Can I just hedge the position instead of selling?

Various hedging strategies exist, including covered calls, protective puts, and prepaid variable forwards. Each has tradeoffs in terms of cost, tax treatment, and effectiveness. Hedging can be a useful complement to diversification but rarely replaces it as a long term strategy. Hedges are time limited and have ongoing costs. Diversification is permanent.

What to Do Right Now

If you have meaningful equity exposure to your employer, the most useful thing you can do is calculate exactly how concentrated you are. Add up the total value of your company stock holdings across all sources, including vested RSUs, exercised options, ESPP shares, 401(k) holdings if applicable, and any company stock held in other accounts. Compare that number to your total investable assets.

If the percentage surprises you, that's the signal to build a diversification plan rather than continuing to let the exposure grow.

This is exactly the kind of work I do with executives in the pharma and life sciences space, typically in coordination with your existing CPA and estate attorney. I hold the CFP®, CIMA®, and CPWA® designations, with the latter two earned through the Yale School of Management. I work with a small number of clients by design, which means when you engage with me, you get my full attention on these decisions.

I'm based in Chester, NJ and serve executives throughout Morris County, Somerset County, and the broader northern New Jersey corridor. If you have meaningful company stock exposure and no clear plan for managing it, reach out directly.

Bill Clinton, CFP®, CIMA®, CPWA® Riverstone Wealth Planners Chester, NJ 908-888-6906 Bill.Clinton@LPL.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.