Avoiding the Surprise Tax Bill: Why Executive Withholding Almost Always Falls Short

Avoiding the Surprise Tax Bill: Why Executive Withholding Almost Always Falls Short

If you've been an executive long enough, you've probably had at least one April that didn't go the way you expected. You assumed taxes were being withheld appropriately throughout the year. Your CPA filed the return. And the bottom line was a number that surprised you, often by tens of thousands of dollars, sometimes more.

Most executives experience this once and assume it was bad luck. It almost never is. It's a structural problem in how withholding works for high earners with complex compensation, and it's one of the most preventable issues in executive financial planning.

Why Withholding Falls Short

The reason executive withholding is consistently inadequate comes down to how the IRS treats different types of income.

Your base salary is withheld at a rate calculated against your annual salary using the standard withholding tables. For most executives that math works reasonably well in isolation.

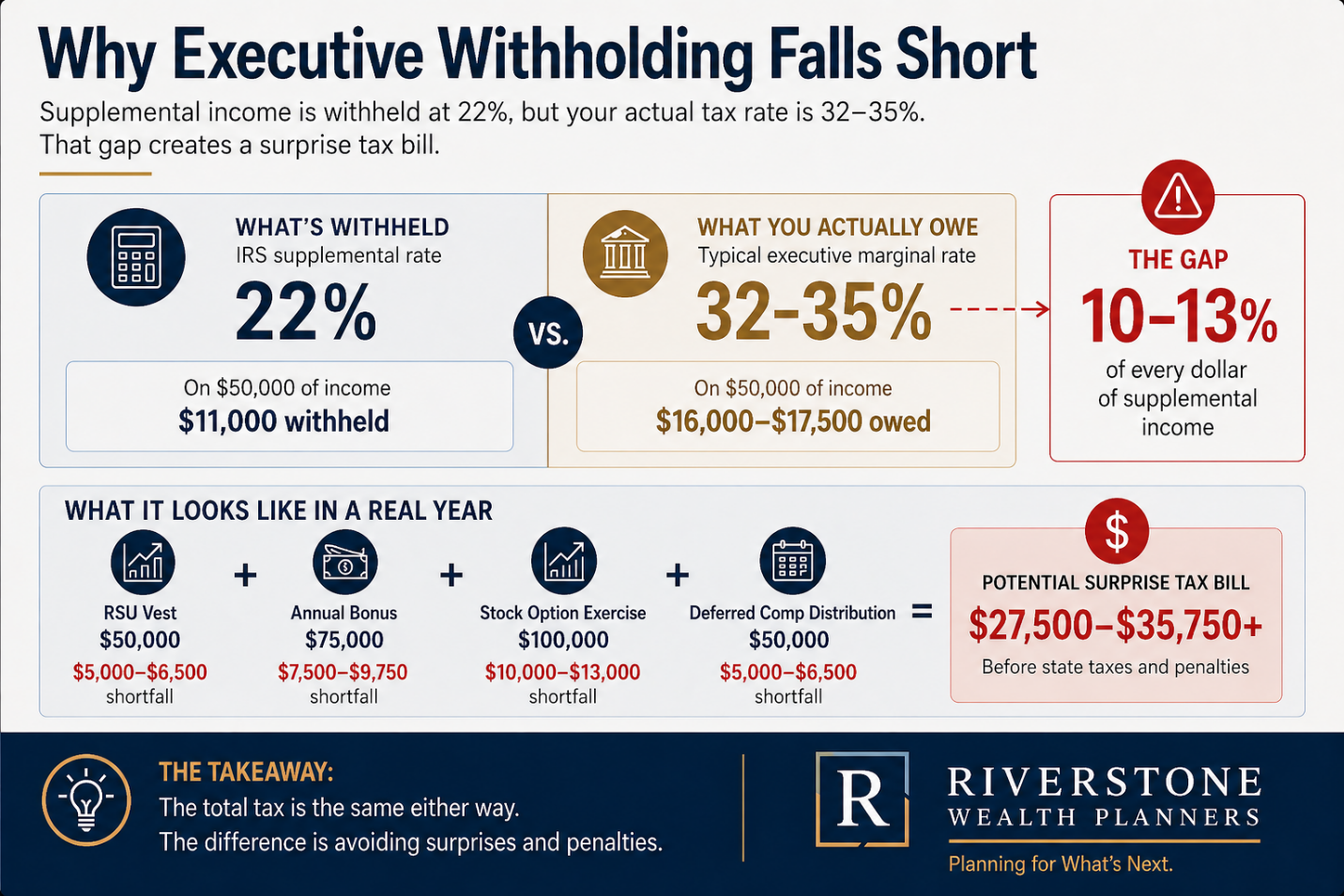

The problem is everything else. Bonus payments, RSU vesting, non-qualified stock option exercises, and deferred compensation distributions are all classified as supplemental wages. The default federal withholding rate on supplemental wages is 22%. That number was set by the IRS as a flat rate intended to capture taxes on bonuses for the average earner.

For a director or VP level executive at a major pharma company, your actual marginal federal tax rate is almost certainly 32% or 35%. The gap between what's being withheld and what you actually owe is 10 to 13 percentage points on every dollar of supplemental income.

On a single $50,000 RSU vest, that's a $5,000 to $6,500 shortfall. On a year with multiple vesting events, an option exercise, and a bonus, the numbers add up quickly. Add New Jersey state income tax to the federal gap and the picture gets worse.

Why It Gets Worse Over Time

The withholding gap compounds because executive compensation grows in ways that withholding doesn't keep up with. Early in your career your supplemental income is modest and the 22% withholding is reasonably close to your marginal rate. As you advance, your bonus grows, your equity grants increase, and your overall compensation profile shifts from mostly base salary to a meaningful percentage in supplemental forms.

By the time you're a director or VP, the majority of your annual compensation is often delivered in forms that are systematically under-withheld. The system that worked when you were earning $200,000 doesn't work when you're earning $500,000 or $750,000.

Most executives don't recalibrate. They assume what worked before continues to work. It usually doesn't.

The Penalty Layer

The IRS doesn't just want their money. They want it on time. If your withholding plus estimated payments falls short of certain thresholds, you owe an underpayment penalty in addition to the balance due. The safe harbor rules require you to either pay at least 110% of your prior year's tax liability through withholding and estimates, or 90% of the current year's actual liability.

For executives whose income is rising year over year, the prior year safe harbor is often achievable but creates its own problem. Paying 110% of last year's tax liability through withholding alone might not happen automatically because your withholding is based on current income, not last year's number. If your income is materially higher this year and you don't make adjustments, you can both owe a large balance and incur penalties for underpaying along the way.

What Experience Has Taught Me

A few things have become clear from working with executives on these issues over the years.

First, the surprise tax bill is almost never the result of one specific decision. It's the result of multiple income events happening across a single calendar year without anyone running the math in advance. RSUs vest, options get exercised, a bonus lands, deferred comp distributes. Each one is under withheld. Stack them and the gap becomes substantial.

Second, the fix is not complicated, but it does require attention. A mid year tax projection done in June or July tells you almost everything you need to know. By that point you can see what's already happened year to date, you know what's scheduled for the rest of the year, and you have time to adjust withholding or make estimated payments before the year ends.

Third, this work is done in coordination with your CPA. We model the tax picture together, identify gaps, and decide whether the right answer is adjusting your W4, making quarterly estimates, or some combination. Your CPA does the return. We make sure there are no surprises by the time the return gets prepared.

Fourth, the executives who avoid surprise tax bills aren't paying more in taxes overall. They're just spreading the payments correctly throughout the year and avoiding penalties. The total liability is the same. The experience is completely different.

Common Questions About Executive Tax Withholding

Why is my withholding too low if my employer is using IRS guidelines?

Your employer is using the IRS supplemental wage withholding rate of 22%, which is correct under the rules. The issue is that this rate was designed for the average earner, not for executives in the 32% or 35% bracket. Your employer is following the rules. The rules just don't fit your situation.

Can I ask for higher withholding on RSU vests?

Some companies allow executives to elect a higher supplemental withholding rate of 37% on equity events. This option isn't always offered or visible in the standard enrollment portals. It's worth asking your benefits team specifically whether it's available. Even if it's not, you can adjust your W4 withholding on regular pay to compensate.

How do estimated tax payments work?

Estimated payments are quarterly tax payments made directly to the IRS to cover income that isn't sufficiently withheld. For executives with significant supplemental income, estimated payments are often necessary to avoid underpayment penalties. Your CPA can calculate the right amount based on a mid year projection.

What's the safe harbor and how do I meet it?

The safe harbor is the threshold that protects you from underpayment penalties. You generally need to have paid in either 110% of last year's total tax liability through a combination of withholding and estimates, or 90% of the current year's actual liability. For most executives the prior year safe harbor is the easier target because the number is known.

Should I just have my CPA handle this?

Your CPA prepares your return and can run projections, but most CPAs are reactive rather than proactive. They tell you what already happened. The planning work, including timing decisions on options, distribution elections on deferred compensation, and coordination across all your income sources, happens before the year ends. That's where an advisor focused on executive compensation adds value alongside your CPA.

What to Do Right Now

If you've been surprised by your tax bill in any of the last few years, that's a signal to get ahead of the problem before this year ends. Pull your year to date pay stubs and identify what's already vested, exercised, or distributed. Estimate what's still scheduled to happen between now and December. Run a rough projection of total income and compare it to what's been withheld so far.

If the gap is meaningful, there's still time to fix it. A withholding adjustment, an estimated payment, or both can close the gap before April becomes a problem.

This is exactly the kind of work I do with executives in the pharma and life sciences space, typically in coordination with your existing CPA. I hold the CFP®, CIMA®, and CPWA® designations, with the latter two earned through the Yale School of Management. I work with a small number of clients by design, which means when you engage with me, you get my full attention on these decisions.

I'm based in Chester, NJ and serve executives throughout Morris County, Somerset County, and the broader northern New Jersey corridor. If your withholding picture has gotten complicated enough that you want a second set of eyes on it, reach out directly.

Bill Clinton, CFP®, CIMA®, CPWA® Riverstone Wealth Planners Chester, NJ 908-888-6906 Bill.Clinton@LPL.com

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.