You Don't Want Your Parents' Advisor: A guide for women inheriting from a parent

The woman I'm going to describe in this piece isn't one person. She's a pattern. I've worked with enough women in her situation that I can describe her clearly without describing anyone in particular. The details are blended to protect privacy. The pattern is real.

She's 58. Her second parent died a few months ago. Her father went first, years earlier; her mother held on until last winter. She's an executor, or she has a sibling who is. There's an attorney involved. The estate is mostly settled. She's about to receive somewhere between one and a half and five million dollars, typically a mix of an inherited IRA, a brokerage account, and her share of a house that's already on the market. She reached out to me on her own, usually through a friend or her attorney, occasionally after finding the practice online.

The first thing she said when we sat down was this: "I'm inheriting money. My parents work with an advisor. I want to find someone new."

That sentence is what I want to talk about in this piece. Not the money. The sentence. Because the woman who says it is asking for something specific, and most of the time she doesn't yet know everything she's actually asking for. She thinks she's looking for an investment advisor. She's looking for something bigger than that, and she'll know it when she finds it.

What follows is a description of what that bigger thing actually is. What the work looks like, what the first six months feel like, and what changes when she finally sees the plan that ties it all together. I've written this for two readers. The woman herself, if she's the one who found it. And the friend, attorney, or family member who handed it to her because they knew she needed it.

Before I describe her in more detail, one thing about why I'm the one writing this. I've now worked with many women in exactly this situation, across the full arc of the work. From the first overwhelmed meeting through the plan reveal through the years that follow. Some of those relationships are now five, six, seven years deep. I've been side by side with these women through every part of the process, including the parts that don't show up in marketing materials. The market drops. The second wave of grief. The decision to retire earlier than expected. The phone call about whether to help an adult child or hold the line. The pattern I'm describing in this paper isn't theoretical. It's something I've watched unfold, more than once.

Why Not Your Parents' Advisor

Let's stay on that sentence for a minute. "I want to find someone new."

She doesn't say it harshly. She's usually warm, businesslike, sometimes apologetic about it. But she's clear. She doesn't want to inherit her parents' advisor along with her parents' money. And she's right.

There's nothing wrong with the advisor who served her parents well for twenty or thirty years. That person likely did good work. But she is not her parents. Her tax situation is different. Her timeline is different. Her career, her household, her marriage, her relationship with money. All of it is hers, not theirs. The advisor who knew her father's risk tolerance and her mother's questions does not know hers. He knows the version of her that showed up at the holiday lunch a few times. That's not the same as knowing her.

She also watched something growing up that she's quietly determined not to repeat. She watched her mother defer. She watched her father make the financial decisions and her mother nod along, or she watched the reverse. Either way, she watched. And whatever she watched, she's not interested in being a continuation of it. She wants her own person. Someone whose first conversation is with her, not a continuation of someone else's relationship.

There's another piece of this that comes up almost every time, even though it takes a few meetings before she says it out loud. She's just buried her parents. She doesn't want to build a new financial relationship with someone who's going to retire in five years and hand her off to a junior advisor she's never met. She wants to know that when she hires me, she's hiring me. Not a name on a door that will eventually belong to someone else. The fact that I'm mid-career, not late-career, matters to her. She rarely says it that directly. But it's there, and it's part of why she's looking for someone new.

There's a third piece too, and it's worth naming. She doesn't want the same advisor as her siblings. Even if her parents' advisor is excellent. Even if her brother already moved his accounts over and likes the guy. She wants someone who sees her individually, not as one-third of her parents' estate. She wants to be a person, not a file inside a family.

All three instincts are correct. You wouldn't keep your parents' wallpaper. You don't have to keep their advisor. What she needs is not a continuation. It's a beginning.

What She Thinks She Needs vs. What She Actually Needs

When she walks in, she usually has three questions in her head. They cycle.

What do I do with this money? What about taxes? What about large bills?

Those are the right questions. They're the questions any reasonable person would have. But they're also surface questions, and the work that needs to be done sits underneath them. She thinks she's looking for an investment advisor, someone to tell her which funds to be in, which stocks to sell, what allocation makes sense for her age. That's a real question and we'll get to it. But it's not the first question. It's not even in the top three.

The first question is: what is this money actually for? Not in a sentimental sense. In a structural sense. Is it retirement funding? Is it her kids' college? Is it a beach house she's been thinking about for ten years? Is it a margin of safety that lets her stop working three years earlier than she planned? Is it some combination? Until that's clear, every other decision is being made in the dark.

The second question is: what's the order? She has an inherited IRA, a brokerage account, and proceeds from a house sale arriving on different timelines. Each one behaves differently for tax purposes. Each one has its own clock. The order in which she touches them, which she pulls from first, which she leaves alone, which she repositions, which she ignores, matters more than the investment choice inside any one of them. Most heirs don't know this. Most advisors don't slow down enough to explain it.

The third question is: what changes about her own life? Her own retirement plan just shifted. Her own estate plan just got more complex. Her tax bracket may have changed for the next ten years. Her insurance needs may have changed. Her ability to help her own kids may have changed. The inheritance is not a side event in her financial life. It's a re-architecture of it.

What she needs, in other words, is not an investment advisor. She needs what I've written about elsewhere as a Personal CFO. Someone who looks at her entire financial life as one system, sees how the inheritance changes that system, and helps her make decisions in the right order. The investment piece is one of the answers. It's not the question.

I sometimes describe it to clients this way. I want to be your 911 and your 411. The 911 part means when something happens that you don't know how to handle, a tax notice you don't understand, a market drop that's scaring you, a financial pressure inside the family you don't know how to navigate, you call me first. The 411 part means when you need information you don't have, what does this account do, what does this letter mean, what should I be thinking about for next year, you call me first. Both numbers. Same advisor. The point is that you don't have to figure out who to call. You call me, and we figure out the answer together.

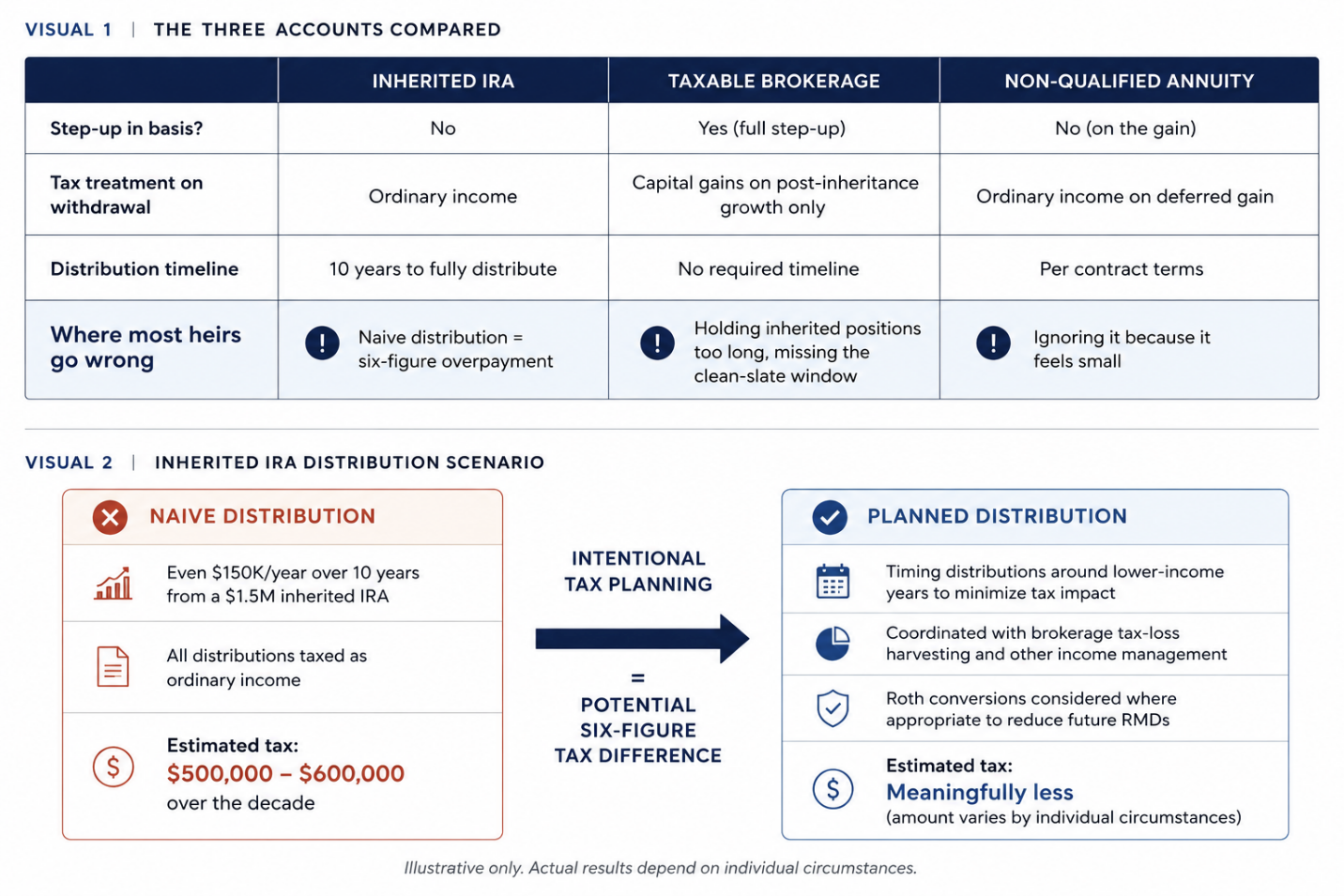

The Three Accounts That Behave Nothing Alike

Here's the thing most people don't realize when they inherit money. The kind of account it's coming from matters more than the investments inside it.

She doesn't know this on day one. She thinks she's inheriting "investments," one big pool of money split across a few statements. In her mind, the work is figuring out the right allocation, the right funds, the right risk level. That's not wrong, but it's a long way down the priority list. The first conversation we have is about what type of account each piece of the inheritance is sitting in, because each one behaves completely differently under the tax code, and the order in which she touches them over the next decade determines how much of this money she actually keeps.

Let's walk through the three accounts that typically arrive.

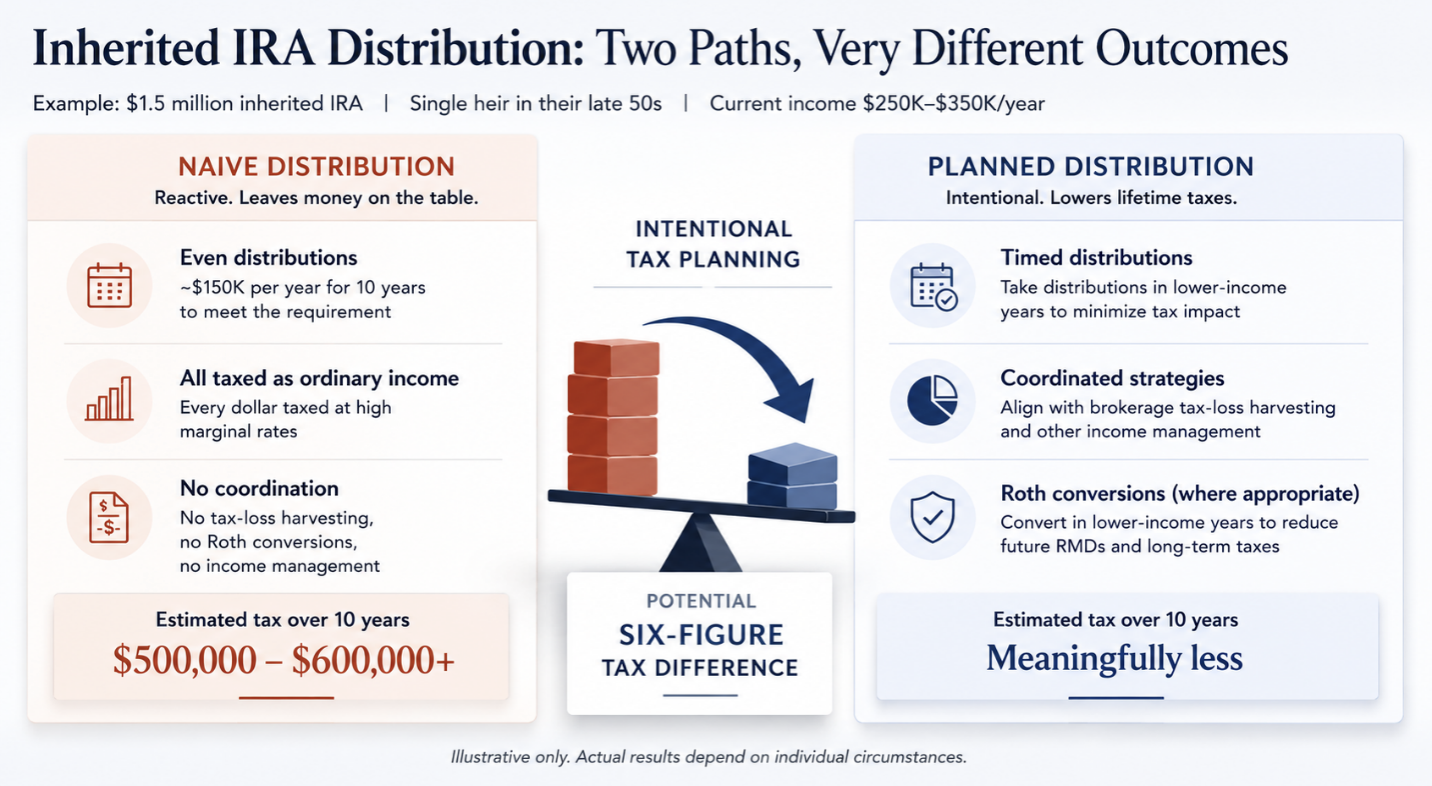

The Inherited IRA. This is the account that most people get wrong, and it's also the largest tax exposure she's likely to face. Under current law, an inherited IRA from a parent has to be fully distributed within ten years. Every dollar she pulls out is ordinary income, taxed at her marginal rate. There's no spreading it over her lifetime the way her parent could. There's no stretching it across her children. Ten years, and it's empty.

Here's where the math gets sharp. The women who walk into my office are usually in their peak earning years. She might be making $250,000 or $350,000 in her own career. She's already in a high federal bracket and she lives in New Jersey, which adds a state layer on top. If she inherits a $1.5 million IRA and pulls it out evenly over ten years, she's stacking $150,000 of additional ordinary income on top of her W-2 every year, pushing her into the 32% or 35% federal bracket, plus New Jersey. Done thoughtlessly, that's a tax bill of roughly $500,000 to $600,000 over the decade. Done thoughtfully, by timing distributions around lower-income years, coordinating with Roth conversions where appropriate, accelerating in down-market years, and using tax-loss harvesting in her brokerage account to offset, the same withdrawal can cost meaningfully less. Six figures of difference is not unusual.

This is not theoretical. This is the single largest planning decision she's going to make, and it has to start the year she inherits, not the year she retires.

The Brokerage Account. The taxable brokerage account works the opposite way. When she inherits it, she gets what's called a step-up in basis. Her parent might have bought Apple at $20 a share thirty years ago. The embedded gain, the difference between what they paid and what it's worth today, is wiped clean at the date of death. She inherits those shares at their current market value. If she sold them the next day, there would be little or no capital gains tax.

Most heirs don't know this, and the practical implication is enormous. The legacy individual stocks her parents accumulated over decades, the Microsofts, the Apples, the Exxons, the General Electrics, can be repositioned without the tax cost that her parents would have faced. If those positions are too concentrated, too narrow, or too tied to her parent's old employer, she has a clean opportunity to diversify. That window won't stay open forever. The longer she holds the inherited positions and lets new gains accumulate, the more taxable the eventual rebalancing becomes.

This is the part of the inheritance where she has the most flexibility and the least urgency, which is exactly why most heirs leave it alone too long. The brokerage account is where calm, deliberate work pays off.

The Non-Qualified Annuity. The third account doesn't always show up, but when it does it surprises people. Many parents of this generation bought non-qualified annuities in their 60s and 70s, sometimes through their old advisor, sometimes through an insurance agent. The accounts are usually small relative to the IRA and the brokerage account. But they have a rule that catches almost everyone off guard.

The gain inside the annuity does not get a step-up in basis. Whatever growth accumulated inside that contract while her parent was alive is still fully taxable as ordinary income when it comes out, to her. Unlike the brokerage account, there's no clean slate. Unlike the IRA, there's a different set of distribution rules. Each annuity contract has its own terms, its own surrender schedule, its own beneficiary options. The right move depends on the specific contract, her own tax situation, and how the annuity fits with everything else.

The annuity is usually the account she's most tempted to ignore. It feels like a small piece of the puzzle, it was something her parent set up a long time ago, and the paperwork is intimidating. Ignoring it is a mistake. The deferred gain inside it is a tax obligation she will eventually pay, and the question is whether she pays it on her schedule or on the contract's.

The point of walking through all three is this: most heirs think about their inheritance as a single number. The estate attorney sends a letter that says "your share is approximately two million dollars," and that's how she carries it in her head. But that number is doing a lot of hiding. The three accounts inside it behave nothing alike. The right move on the IRA is different from the right move on the brokerage account, which is different from the right move on the annuity. The sequence matters. The timing matters. The interaction with her own income and her own retirement plan matters.

This is the single biggest reason most heirs are running the math backwards. They protect the brokerage gains they don't need to protect and they panic-pull from the IRA they should be more careful with. Or they leave the annuity untouched for years because "Mom had it forever," not realizing the tax clock is still running inside it.

The first job of the plan is to fix this. Not the investment allocation. The architecture.

What the First Six Months Actually Look Like

Most marketing pieces describe the work in vague terms. Comprehensive planning. Holistic approach. Tailored strategies. Those phrases are everywhere and they don't tell you anything. So let me describe what actually happens in the first six months, in plain language.

The first meeting is mostly gathering. I want to see what she has. Account statements, beneficiary designations, the will or trust documents, her own retirement account information, her tax returns from the last two years, her current household budget if she has one, the estate paperwork from the attorney. Some women arrive with this in a neat folder. Some arrive with most of it in their head and the rest scattered across email inboxes and shoeboxes. Either is fine. We work with what's there.

The starting point varies more than people expect. Some parents had a longtime advisor and one or two clean account statements. Others spent fifty years assembling a financial life on their own. In those cases, the inheritance arrives in pieces. A 401(k) from a job the parent left in 1992. An old brokerage account from a custodian that's been through several mergers. Two custodial accounts at a custodian that's been acquired twice since they were opened. Paper savings bonds in a drawer. A credit union account in another state. Three IRAs at three different places, opened years apart, possibly with outdated beneficiaries. When this is the situation, the first part of the work isn't planning. It's archaeology. We find all of it, we consolidate what makes sense to consolidate, we update the beneficiaries that should have been updated years ago, and we get the picture clean enough that real planning becomes possible. This takes longer than people expect. It also relieves a quiet anxiety she's been carrying since her parent died, the worry that she'll discover another account in six months and the planning will have to start over.

Sometimes she arrives with the right people already in place. An estate attorney who handled the will. A CPA who's been doing her returns for years. If those people are good, we work together. I coordinate with them on the planning decisions, and they handle the legal and tax filing work on their side. If those people aren't a fit, or if she doesn't have them yet, I introduce her to professionals I've worked with for years and trust. A short list of estate attorneys and CPAs in the area who I know personally, whose work I've seen, and who treat clients the way I'd want to be treated myself. Some women come to me first, before they've found their attorney or their accountant, and we build the team from there. Either way, by the end of the first six months, she has a small professional team around her. Not just an advisor, but a coordinated group of people whose work fits together.

The first operational step is account titling. Money cannot move into a plan until the accounts are in her name. The inherited IRA needs to be set up as a beneficiary IRA in her name with her late parent's information attached. The brokerage account needs to be retitled or transferred. The annuity contract needs a beneficiary election. These are paperwork steps, but they take longer than people expect, and they need to happen before any planning decisions get implemented.

While the paperwork is moving, we're building the plan. This is the work that takes the most time and matters the most. We look at her own retirement picture, her tax situation over the next ten years, her cash flow, her debt if any, her own estate plan, and her goals for the inheritance. We model out scenarios. What happens if she keeps working until 65? What happens if she stops at 62? What changes if she pays off her mortgage with part of the brokerage account? What changes if she doesn't? What does the inherited IRA distribution schedule look like under each scenario? When does she actually have enough?

By the third or fourth meeting, the plan is ready to walk through. We sit with it. She asks questions. She pushes on assumptions. She tells me what feels right and what doesn't. We adjust.

Some decisions get made early. If she has high-interest debt, a credit card balance, a personal loan, anything with an interest rate that's outrunning what a portfolio can reasonably earn, that gets addressed first. The math is rarely close. Paying off high-interest debt is usually the cleanest dollar she can spend.

Other decisions get deliberately deferred. The most common one is gifting to her own children. She often walks in wanting to immediately help her kids. Pay off student loans, fund a wedding, help with a down payment on a first house. My job in the first six months is usually to slow that conversation down, not stop it. Generosity is one of the best things she can do with this money, eventually. But early generosity, made before the plan is built, is how inheritances disappear. We come back to the gifting question in year two, when the plan is settled and we know what she can actually afford to give.

The cadence in the first six months is heavier than most clients expect. We're typically meeting four to five times, an hour each. This isn't a sales process. It's the time it actually takes to build something this important right. After the first six months, the cadence settles down. Two to three meetings a year is usually the right rhythm once the foundation is in place.

Some women hear "four to five meetings" and feel overwhelmed before we've even started. If that's you, I want you to know we go at the pace that feels right to you, not the pace that's convenient for me. There's no rush. The plan still gets built well if it takes seven meetings instead of four. The accounts still get titled. The tax strategy still gets set up. If you need more space between meetings, we take more space. If you need to slow down on a specific decision, we slow down. Nothing about this process is on a clock that someone else set. The only deadline that matters is the inherited IRA distribution clock, and that gives us ten years, not ten weeks.

The husband's role varies. Sometimes there isn't one. Sometimes he's intentionally not involved, by her preference or his. Sometimes he comes to meetings to listen, and he's there to support without driving the conversation. And sometimes the inheritance is large enough, or her life is intertwined enough with his, that the plan we build naturally grows to cover both of them. In those cases, I'm doing financial planning for the household, with her at the center because she's the one who inherited and she's the one who set this in motion, but with him fully involved because the decisions we're making touch his life too. The frame stays the same in every version of this. Her parents. Her inheritance. Her decisions. Whether he's absent, observing, or fully engaged, this work begins with her.

Before You Ask About Cost

Every woman who sits across from me has this question in her head, and most of them are reluctant to ask it out loud. So I bring it up first.

The question is: what is this going to cost me?

The honest answer is that it depends on what we end up doing together, and I'd rather walk you through the options than quote you a number that doesn't fit your situation. I offer a few different fee structures. There's an asset-based fee, where the cost is a percentage of what I'm managing. There's a flat project fee, where we agree on a price for a specific piece of work. There's an hourly rate for clients who only want a consultation. And there's a retainer model for ongoing planning without investment management. You can choose the one that fits how you want to work with me.

Most clients end up choosing the asset-based fee, and I'll tell you why. For the work I do with inheritors, the ongoing tax planning over the 10-year IRA window, the multiple meetings in the first six months, the proactive outreach when the market moves, the lifestyle modeling we do as her plan evolves, the asset-based fee tends to be the cleanest structure. It aligns my incentive with hers. When her wealth grows, I do better. When it doesn't, I don't. There's no meter running during phone calls. There's no separate bill for each tax projection. It's one fee that covers everything.

But it's not the only option, and it's not the right option for every situation. We'll talk through it in the first meeting. You'll know what you're paying for before you commit to anything, and there will be no surprises. If you ever decide it's not the right fit, you can leave. There are no long-term contracts.

That conversation happens early. Before any documents get signed. Before any accounts move. You should know exactly what you're getting into.

The Moment Everything Changes

Most clients tell me the moment everything changes isn't when the inheritance lands in their account. It's when they see the plan.

There's a specific meeting where this happens. Usually the third or fourth one, after the documents have been gathered and the accounts have been titled and the modeling has been done. I walk her through the full plan on screen. Her own retirement projection, the inherited IRA distribution schedule over ten years, the tax implications by year, the cash flow if she keeps working and the cash flow if she stops, the trajectory of the portfolio under different assumptions, the answers to the questions she's been carrying for months.

Somewhere in that meeting, almost always, she says some version of the same thing.

"Oh my gosh, I get it."

That's the turn. It's not gradual. It's a specific moment. The questions stop cycling. The fog she's been carrying since her parent died, the one she didn't realize she was carrying until it lifted, lifts. She can see the path. She knows what she's doing. She knows what the next ten years look like, in numbers and in life, and the not-knowing was costing her more than she realized.

The relief is physical. I've watched it happen across a conference table more times than I can count. Shoulders drop. She leans back. Sometimes she cries a little, in the way you cry when something heavy you've been carrying gets put down. The meeting that follows the plan reveal is almost always a different meeting than the one before it. She's no longer the person who walked into my office with a folder and a list of worries. She's the person who has a plan.

There's one more thing worth saying about the turn. It usually has to be tested. A few months after the plan reveal, the market moves. It always does. And when it moves, the paper losses on a now-larger portfolio are bigger than anything she's experienced before. A five percent drop on a two-and-a-half million dollar portfolio is a paper loss of $125,000, bigger, in a single afternoon, than most people's annual salary. The first time this happens, the relief she earned at the plan reveal is suddenly fragile.

This is where most advisors quietly fail their clients. They don't call. They wait for the client to call them. And the client, alone in front of her account balance, decides she made a mistake.

The work in those moments is different from the work in the plan-building. It's the phone call I make to her the day of the drop, not the week after. It's the conversation about what the plan already accounts for. It's the reminder that the projections we built assumed exactly this kind of volatility, and the long-term math hasn't changed. That second conversation, the one most advisors don't make, is where the trust actually gets cemented. Not when things are easy. When they aren't.

Two Versions of This Story

I want to be direct about something most marketing pieces skip.

The women who walk into my office with an inheritance arrive in different financial situations, and the work I do for each is different.

For some, the inheritance is an accelerant. They've built a solid foundation through their working years. Their own retirement is on track or close to it. Their household is in good shape. The inheritance changes the timeline of what was already possible. The plan opens options. An earlier retirement, the beach condo she's been thinking about for ten years, the grandchildren's 529s, the meaningful gift to a charity her parent cared about. For these women, the work is about sequence and tax efficiency. The plan tells her how much earlier she can stop working, and how to keep more of what she's inheriting along the way.

For others, the inheritance arrives at a more complicated moment. Life doesn't always go the way we hoped in our thirties and forties. Careers shift. Marriages end. Expensive towns get more expensive. The breathing room we expected never quite arrived. These women walk in carrying a heavier load than the first group, and they know it before I do.

For them, the inheritance is something different. It's a chance to build the retirement that wasn't going to happen otherwise. With a real plan, including, sometimes, a real budget, it can become the foundation that was missing. Without one, it can disappear into the same patterns that made the road hard in the first place.

I tell you both versions because women in this situation deserve to be seen accurately, not flattered. The plan tells the truth. Whichever version you're closer to, knowing where you actually stand is the foundation everything else gets built on. There's no version of this work that begins with a story that isn't honest about where the starting line actually is.

Where She Is, A Few Years In

I'm now in year five, six, and seven with some of the women I started this work with. The inheritance that felt overwhelming when they first sat down across from me is now just part of how their lives function. They've taken trips they couldn't have taken before. They've made decisions about retirement that they couldn't have considered before. They've watched the market move, up and down, more than once, and we've handled it together. They've called me with the second wave of questions that nobody warned them was coming, and we've worked through those too.

What I want you to know is that this isn't theoretical. The arc I'm describing, from the overwhelmed first meeting through the plan reveal through the years that follow, is something I've now lived through with multiple clients, in full cycle. I know what year one looks like because I've sat in the chair across from her in year one. I know what year five looks like because I've sat there in year five, with the same person. The pattern I'm describing in this paper isn't something I'm projecting forward. It's something I've watched unfold.

A year or two after the plan is in place, the meetings change.

She's no longer asking what to do. She's asking what's next. The questions shift from reactive to forward-looking. Should I retire at 63 instead of 65? What if we modeled a second home at the shore? My daughter is getting married next spring, what's the right way to help with the wedding? I've been thinking about a board seat at the foundation my mother supported, can we plan around that? These are the questions of a woman who is no longer in survival mode. She's designing a life.

The plan evolves with her. The inherited IRA distributions, which felt overwhelming in year one, become routine. In some cases we set them up as monthly transfers, which gives her an additional income stream she can count on. The brokerage account, repositioned thoughtfully in the first eighteen months, has done its job and continues to do it. The annuity, if there was one, has been handled. Her own retirement accounts are integrated into the larger plan. The cash flow projections, which started as a way to answer "can I stop working?", become a tool for "what do I want to do next?"

Some women retire earlier than they thought possible. Some keep working because they want to, not because they have to, and that distinction matters more to them than they expected. Some begin giving meaningfully to causes their parent cared about, and find that the gifting itself becomes part of how they process the grief. Some help their adult children in ways the plan allows for now that it couldn't allow for in year one. Some buy the beach condo. Some pay off the mortgage and text me a photo of the closing statement.

Her relationship to the money also changes. In year one, it was an emotional object. It carried her parent in it. By year three, it's becoming something else. Still meaningful, but less heavy. She refers to it differently. Less "Mom's money" and more "the portfolio" or just "my plan." That shift is not disloyalty. It's integration. The money has become hers, in the same way the grief has become part of her life rather than the whole of it.

She also starts referring people. Almost always without being asked. A friend going through a divorce. A sister-in-law whose father just died. A colleague at her firm whose mother has been declining. The referral usually comes with some version of the same sentence: "I told her she needs to talk to you. I wish I'd found you sooner."

That last line shows up often enough that I've stopped being surprised by it.

Let me come back to the sentence I opened this piece with.

"I'm inheriting money. My parents work with an advisor. I want to find someone new."

Whichever woman is reading this, the one whose inheritance accelerates a life that was already on track, or the one whose inheritance is the chance to build a life that wasn't, the work is the same in one important way. It starts with telling the truth about where you actually are. The plan does that. Then we build forward from there.

The most common thing women say to me a year or two into this work is some version of "I wish I had done this sooner." I don't tell you that as a sales line. I tell you because the women who say it are usually surprised by how much lighter their lives became once they stopped carrying the questions alone. The not-knowing was costing them more than they realized.

If you're reading this and you're in the middle of this transition, or you can see it coming, the first conversation is free, and there's no pressure attached to it. I'd rather spend an hour with you and never hear from you again than have you make decisions of this size without someone honest in the room with you. If we're a fit, we'll know it. If we're not, you'll walk away with a clearer picture than you came in with, and that's worth something on its own.

If you're a friend, an attorney, or a family member who handed this to a woman you care about because you knew she needed it, thank you. The reason she's reading this at all is because you saw her. That matters more than you know.

Bill Clinton, CFP®, CIMA®, CPWA® Riverstone Wealth Planners Chester, New Jersey riverstonewealthplanners.com